Forget the drop in the dollar value of China’s imports in July, the important numbers were the bumper purchases of major commodities including crude oil, coal, iron ore and copper.

The 5.6% drop in the dollar value of July imports is almost irrelevant and most likely a reflection of lower commodity prices rather than any weakness in the Chinese economy.

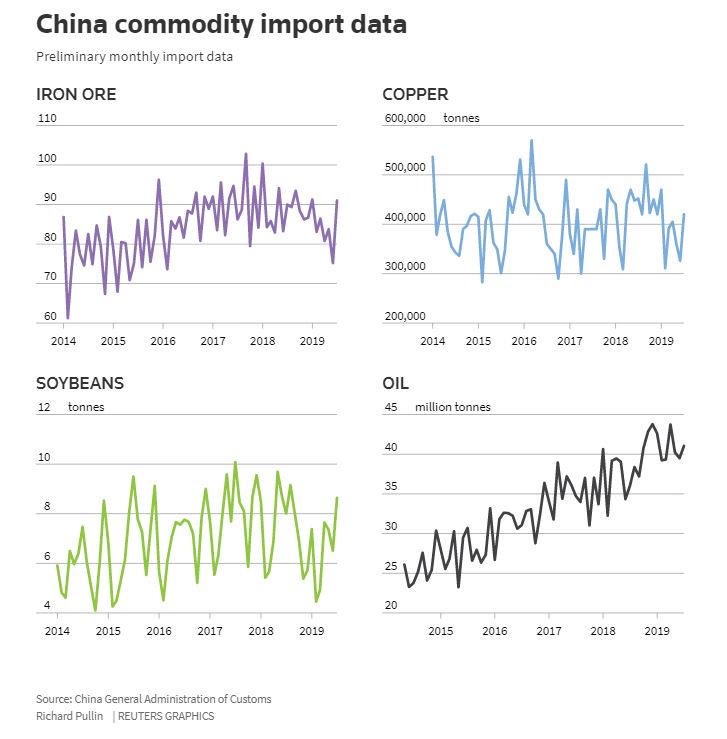

What is worth looking at is the 21% month-on-month jump in iron ore imports to 91.02 million tonnes in July, the highest since January.

Or how about the 21% rise in coal imports to 32.89 million tonnes, also the highest since January.

In fact, there’s a bit of a pattern developing, as unwrought copper imports of 420,000 tonnes, up 29% from June, are also at the highest level since January.

Even more bullish for copper was the 41% surge in imports of ores and concentrates to 2.074 million tonnes in July, the highest on record.

Crude oil was somewhat less impressive, with July’s 9.66 million barrels per day (bpd) only slightly above June’s 9.63 million bpd, however, this was up 14% from July last year.

While there are temporary factors that may explain some of the strength in China’s imports of major commodities, it’s becoming increasingly hard to sustain a case that they are being adversely affected by the ongoing trade dispute with the United States.

Some of the strength in July is likely a catch-up from some prior months of softness, especially in iron ore, where supply has been affected by a mine dam disaster in Brazil forcing safety checks and a tropical cyclone in Australia.

But steel mills wouldn’t be buying iron ore if they didn’t believe they could make money, so the rise in July is a sign of confidence for the outlook for steel demand.

Higher electricity demand over the northern summer may have spurred coal demand, but it’s worth noting that the gain in imports came even as customs officials halted or delayed cargo clearances at several ports.

Coal imports may also have been boosted by lower prices making overseas supplies more competitive against domestic output, but the overall message is still the same – if the Chinese don’t think they can use the commodity profitably, they won’t import it.

COPPER SWINGS

The nature of China’s copper demand is also shifting, with a move toward ores and concentrates and away from refined products.

Not only was July a record for imports of ores and concentrates, the first seven months has seen a 10.8% increase in overseas purchases.

In contrast, imports of unwrought copper are down 11.7% in the first seven months, even accounting for July’s resurgence.

The build-out of Chinese copper smelter capacity is driving this dynamic, and this is a structural change that the rest of the global copper market will have to adjust to.

While crude oil imports were only slightly higher in July, natural gas imports, both pipeline and liquefied natural gas (LNG), were 7.89 million tonnes in July, up 4.9% from June and also the highest since January.

Similar to coal, natural gas imports may have been boosted by summer demand, but it’s also worth noting that spot LNG prices fell to their lowest in three years in June, when cargoes for July delivery would have been arranged, and have fallen more since.

It’s not just LNG prices that are down, the benchmark weekly thermal coal price at Australia’s Newcastle Port slipped to the weakest since September 2016 during June, and has fallen further since.

London copper was also weak in June, trading at the lowest since January and subsequently fell to a two-year low on Aug. 8.

Brent crude oil was also coming off the boil in June, dropping to a five-month low of $59.97 a barrel on June 12 and the mild rally since then has not been sustained, with the benchmark light crude ending at $56.23 on Wednesday.

Iron ore was the exception, with prices still rising in June, although they have subsequently started to drop, with renewed trade war fears sparking a 26% slump since they hit a 5-1/2-year high in early July.

What China’s commodity imports appear to be showing is that there is a far degree of resilience in the economy, and that lower commodity prices may act as spur to further buying as they help margins.

Source: Reuters (Editing by Richard Pullin)