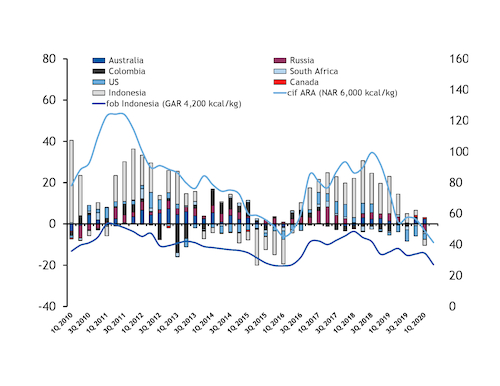

Global thermal coal exports in March recorded their steepest annual decline in more than four years, with further supply adjustments likely in the near term as the market rebalances in the wake of lower prices and demand.

Combined exports from seven of the major coal-producing nations fell by a little more than 5mn t on the year to 84.5mn t in March, based on a combination of customs and shipping data. This was the steepest annual decline since January 2016, when exports fell by 7.7mn t to 62.9mn t.

The contraction in supply in March dragged first-quarter exports down by 7.2mn t on the year to about 243mn t, which was only the second annual decline in quarterly shipments since that start of 2016, following a 3.2mn t drop in the third quarter of last year.

Atlantic suppliers accounted for the vast majority of the global contraction in first-quarter exports, as weak demand and prices in Europe were already driving volumes lower during the early stages of the Covid-19 pandemic. But Indonesian exports were the single-biggest driver of the slump in March and look set to play a leading role in restoring balance to the global market in the near term, as demand wilts because of Covid-19 restrictions.

Russian volumes were hit hardest in the first quarter, falling by 3.1mn t on the year to a two-year low of 41mn t, shipping data show. Russian supply was hit by low demand in its top export market, South Korea, driven by curbs on the use of coal-fired plants, and across the EU, where mild weather and fierce competition from natural gas slashed power-sector demand.

But a weaker ruble means Russia has the potential to compete strongly in Asia-Pacific and may also be able to expand into Turkey, with the Taman port in the Black Sea expected to load its first Capesize shipments this month. Argus forecasts Russian exports to fall by about 7mn t on the year in 2020.

US exports have been in steady decline for more than a year and continued to suffer from weak European demand in the first quarter, with total shipments down by 2.7mn t, at 7.5mn t. Severe restrictions in India are likely to add to exporters' woes in the near term, as the country accounted for about a quarter of total shipments in recent months.

Colombian supply held up better, and exports actually grew in February as an arbitrage to India and Asia-Pacific opened up, but quarterly volumes were still down by 910,000t in January-March. Colombian coal remains competitively priced in Asia-Pacific, but the long shipping distance can make exports less nimble. And the potential for greater competition from Russia in Turkey is another downside risk to demand for Colombian coal.

Recent mining disruption has seen exporters draw heavily on stocks, which may slow the early stages of the recovery in seaborne supply during the second quarter. Argus currently expects US and Colombian exports to fall by about 11mn t and 7mn t, respectively, this year.

South African exports were comparatively robust against its global peers in the first quarter, but have since fallen sharply because of the plunge in coal demand in India, which accounts for 55pc of South African exports. Volumes were down by only 700,000t on the year in January-March, but fell by 2.3mn t in April alone.

South African coal's importance within the Indian industrial sector could support demand as the country eases lockdown measures and moves to stimulate an economic recovery. But exports will also depend on the extent to which suppliers can compete to sell surplus volumes in Vietnam, South Korea and elsewhere, as has already been seen in recent months. South African exports are expected to drop by about 5mn t this year.

Australia bucks the trend

Australia was the only major exporting country to increase supply in the first quarter, with exports climbing by 2.6mn t on the year to 51.8mn t.

Like South African coal, Australian supply weathered the previous downturn in prices and supply in 2015 well, and sunk costs through take-or-pay contracts for the use of rail and port infrastructure may reduce the incentive for producers to slow output in response to lower prices this year.

Australia has also competed strongly in new markets such as Vietnam and accounts for leading shares of the South Korean and Japanese import mixes, where power demand has looked more robust than in other demand hubs during the pandemic. But worsening relations with China pose a downside risk, with rumours of more stringent restrictions on imports of Australian coal from July.

Argus currently expects Australian exports to drop by 3mn t on the year in 2020.

Indonesian exports were down by nearly 3mn t on the year in the first quarter and will probably be hit relatively hard by lower power-sector demand in India during the lockdown. Indonesian coal has historically played a role as a swing supplier and accounted for much of the reduction in supply during the 2015 downturn.

But the government has not so far revised down production targets and the correlation between exports and low-calorific value prices has weakened in recent years, which may suggest supply will be less responsive to tighter margins this time around. Nevertheless, Indonesia relies heavily on China and India as export markets, both of which are making efforts to support their domestic coal sectors at the expense of seaborne supply.

And low high-calorific value prices mean that markets like South Korea are increasingly overlooking Indonesian coal, as Australian, Russian and other grades offer wider margins on an energy-adjusted basis for power generation.

Indonesian exports are expected to fall by about 40mn t this year.

Source: Argus (By Jake Horslen)

Global thermal coal exports vs seaborne prices mn t, $/t